Aurelium Home Loan's Mortgage Process Timeline

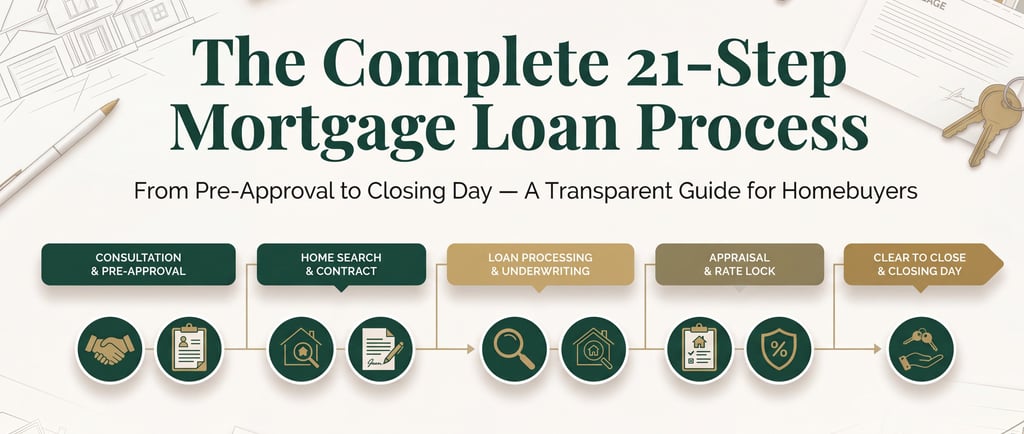

The Complete 21-Step Mortgage Loan Process in Virginia, Maryland & Washington DC

The Complete 21-Step Mortgage Loan Process in Virginia, Maryland & Washington DC

What to Expect When Working With a Mortgage Lender

Buying a home is one of the largest financial decisions you will ever make.

If you’ve been searching for:

how the mortgage process works

steps to buying a house

how to get pre approved for a mortgage

what happens after going under contract

This guide walks you through every stage of the mortgage loan process from consultation to closing.

At Aurelium Home Loans, transparency is foundational. You deserve to know exactly what happens next — at every step.

Step 1 – Discovery Consultation Before Credit Is Pulled

One of the most important steps in the mortgage process is the initial consultation.

Before running credit, a licensed mortgage loan officer should:

Evaluate your financial goals

Review your income structure

Assess your current credit position

Determine whether your goals align with lending guidelines

You should never have your credit pulled “just because.” If a lender asks you to complete a mortgage application without first discussing strategy, that is a red flag.

This step protects you and ensures we move forward intentionally.

Step 2 – Mortgage Pre-Approval Application & Document Review

Once we determine you are ready to move forward, you will complete a formal mortgage pre-approval application.

During this stage:

A soft credit pull is completed

Income and asset documentation is reviewed

Interest rate strategy is discussed

Premiums and lender credits are evaluated

Required disclosures are signed

If you are searching for “how to get pre approved for a mortgage,” this is where it officially begins.

Step 3 – Initial Underwrite & Official Mortgage Pre-Approval Letter

After I have fully assessed your unique credit profile, I will personally structure your loan file and officially submit it to our in-house underwriting department for official review. Durning this time the underwriter reviewing your file may have additional questions or request additional documentation. This is very routine durning the loan process and does not mean that there is anything wrong. The faster we get these items back to the underwriter, the faster we can receive the pre-approval, so I will work very closely with you durning this process to make sure that it goes as smoothly as possible for you.

Once the official review has concluded, if approved, you will receive a formal pre-approval letter designed specifically for you that will directly reflect your buying power to strengthen your offer in competitive markets like Virginia, Maryland, and Washington DC.

Step 4 – Begin Your Home Search With Strategic Clarity

Once your structured pre-approval is issued, you can confidently begin shopping for your future home.

At this stage:

You know your maximum purchase price.

You understand your estimated monthly payment.

You know your projected cash-to-close.

You understand your interest rate strategy options.

This allows you and your real estate agent to write offers with confidence rather than uncertainty.

In competitive markets like Virginia, Maryland, and Washington DC, clarity and speed matter. A properly structured pre-approval gives sellers confidence that your financing is strong and realistic.

Step 5 – Ratified Contract & Formal Loan Activation

Once your offer is accepted and the contract is ratified, the official lender process begins.

At this stage:

A hard credit inquiry is completed.

Your file is submitted through the Automated Underwriting System (AUS).

Credit report fees are paid directly by the borrower through a secure link.

The purchase contract is reviewed in detail.

The AUS evaluates your financial profile against agency guidelines (Fannie Mae, Freddie Mac, FHA, VA, etc.) and issues an approval recommendation.

This step officially transitions your file from pre-approval to full mortgage processing.

Step 6 – Official Loan File Submission to the Lender

Your loan file is formally submitted to the selected lender.

During this time:

Your borrower portal is created.

Your file is indexed within the lender’s system.

Your loan is assigned internally for underwriting.

Portal configuration can take 5–7 business days depending on the lender. However, your file is actively being worked on during this time. There is no pause in processing.

Your documentation is reviewed and organized to ensure a clean underwriting submission.

Step 7 – Loan Estimate & Initial Disclosures

After submission, you will receive your official Loan Estimate (LE).

This document outlines:

Interest rate

Annual Percentage Rate (APR)

Lender fees

Estimated closing costs

Estimated cash to close

Loan program details

You must electronically acknowledge these disclosures to move forward.

It is extremely important to review this document carefully. I walk each client through the Loan Estimate to ensure complete understanding of the numbers.

Transparency at this stage eliminates confusion later.

Step 8 – Initial Underwriting Approval

During this step, your file is actively assigned to the lenders underwriting department and an underwriter is currently assigned to your file to review.

The underwriter evaluates:

Income calculation accuracy

Employment consistency

Asset verification

Debt-to-income ratios

Property eligibility

Credit profile

An initial approval is typically issued at the conclusion of this step with conditions, if any. Conditions are normal and expected in nearly every mortgage file.

Step 9 – Underwriting Conditions & Documentation Requests

Conditions may include requests such as:

Updated pay stubs

Clarification on deposits

Additional bank statements

Letters of explanation

Employment verification updates

These requests are not red flags. They are part of responsible risk management. This is where organization and preparation earlier in the process pay off significantly. Fast response times here are absolutely critical, as the faster we are able to gather all required documentation and return it back to the underwriter, the faster we can move towards getting you the "Clear to Close" as quickly as possible.

Step 10 – Loan Processor Introduction

At this step in the process, your loan processor is officially introduced to you.

Their role and responsibilities within your transaction include:

Collecting requested documentation

Reviewing condition submissions

Communicating with underwriting

Ensuring timelines are maintained

Think of your processor as the operational backbone of your loan once you have been submitted officially to a lender for processing.

Step 11 – Home Inspection

Your home inspection typically occurs within the first 7 days of receiving a ratified contract. Durning this time, your loan file is also in its initial underwrite phase as well with the lender.

The inspection evaluates:

Structural integrity

HVAC systems

Plumbing and electrical

Roof condition

Safety issues

While the lender requires an appraisal, the inspection protects you as the buyer. This step allows you to negotiate repairs or credits if needed.

Step 12 – Contract Addendums (If Applicable)

If negotiations occur after inspection, such as:

Seller-paid repairs

Price adjustments

Seller concessions

An addendum is signed and submitted to the lender. All contractual updates must be reflected in the mortgage file to maintain compliance and accuracy.

Step 13 – Appraisal Ordered

Once the home inspection process has concluded, it is now time to order this appraisal. As the borrower, you will receive an invoice from the mortgage broker for the appraisal and once payment has been received, we will officially order the appraisal for your property.

The appraisal determines:

Fair market value

Property condition

Compliance with loan guidelines

The appraiser is independent and cannot be influenced by buyer, seller, or lender. This protects all parties involved.

Step 14 – Interest Rate Lock

Once you have been initially approved with the lender and your account portal has been successfully configured by the lender we are now ready to lock your interest rate.

Locking your rate:

Protects against market volatility

Secures your pricing

Finalizes your loan structure

Timing the rate lock depends on:

Market conditions

Contract timeline

Risk tolerance

Loan program type

This decision is strategic and discussed thoroughly.

Step 15 – Appraisal Review & Valuation Confirmation

Once the appraisal is received back from the assigned appraiser, the lender will review for accuracy. If the property appraises at or above the purchase price, we proceed normally.

If it appraises below value, options may include:

Renegotiating price

Bringing additional funds

Filing a reconsideration of value

Each scenario is handled carefully and strategically.

Step 16 – Clearing Final Underwriting Conditions

As remaining conditions are satisfied, your loan file continuously moves toward final approval.

At this stage:

All income documentation is finalized

All asset sourcing is verified

Final WVOE's are being completed

Employment verifications are completed

Compliance checks are confirmed

Your loan file is actively being prepared for final sign-off with the lender.

Step 17 – Initial Closing Disclosure (ICD)

As we approach the "Clear to Close" you will receive your Initial Closing Disclosure which is needed at least 3 business days prior to your closing date per federal law.

Important notes:

It is extremely common for numbers on the ICD not to be 100% exact as numbers on the ICD may still fluctuate slightly while title and the lender balance final figures.

Prepaid items such as interest, taxes, and insurance may adjust.

Lender-observed holidays can affect the timing of this delivery.

We plan carefully to avoid delays. I walk you through every line item so there is complete clarity.

Step 18 – Clear to Close

Congratulations you have officially been granted a Clear to Close which means:

All underwriting conditions have been satisfied.

The lender has approved your loan for funding.

No further documentation is required.

This is is a huge accomplishment but it is extremely important that even though you have been granted a "Clear to Close" it is not a guarantee to lend money. 1%-2% of loans don't make it to closing after receiving the "Clear to Close" so it is extremely important to not have any more debt or credit inquiries occur after you have received a "Clear to Close".

Step 19 – Title & Lender Final Balancing

Durning this step, The lender and title company reconcile:

Final payoff figures (if applicable)

Final cash-to-close amount

Recording fees

Escrow adjustments

Accuracy here ensures your closing documents are correct.

Step 20 – Closing Documents Generated

At this time in the process, the lender generates your final closing documents and sends them to the title company.

You will typically receive:

Final Closing Disclosure

Promissory Note

Deed of Trust

Various state-specific documents

You may receive a preliminary copy for review before signing.

Step 21 – Closing Day

You have officially made it to closing and you are ready to take possession of your new property. On closing day:

You sign your final documents.

Funds are disbursed.

The deed is recorded.

You receive your keys to your brand new home.

At this point, you officially become a homeowner.

Why Understanding the Mortgage Loan Process Matters

When borrowers understand the steps of the mortgage process:

Stress decreases

Confidence increases

Surprises are minimized

Decisions become clearer

If you are looking for a mortgage lender in Virginia, Maryland, or Washington DC who prioritizes transparency, structure, and communication, Aurelium Home Loans is built for you.

Ready to Start the Mortgage Pre-Approval Process?

If you’re searching for:

mortgage lender near me

VA loan lender

FHA loan lender

first time home buyer mortgage

mortgage broker in Virginia, Maryland, or DC

Let’s build your mortgage strategy correctly from day one.

- Jake Bumbrey Jr-

Licensed MLO: NMLS #2603530 (VA)

Get In Touch

8401 Mayland Dr #6807

Richmond, VA 23294

Office Hours: Daily 9am-9pm ET

© 2026 Aurelium Home Loans. All rights reserved.

Powered by: